A real-world guide to buying your first home, without the overwhelm.

Let’s be honest. Buying your first home can feel like stepping into a world where everyone else knows the rules, and you’re just trying to figure out what “escrow” means.

If that’s you, take a breath.

This article isn’t about pressure. It’s about clarity. It’s about helping you feel confident, informed, and actually excited about what’s ahead.

Whether you’re six months out or just starting to scroll listings at night thinking, “Could we actually do this?”, you’re in the right place.

Why homeownership matters (beyond the obvious)

Homeownership is more than a monthly payment. It’s stability. It can contribute to long-term wealth building. It’s freedom. And for many first-time buyers, it’s the first step toward financial independence.

1. Stability you can plan around

Rent goes up. It just does. A fixed-rate mortgage? Your principal and interest payment stays the same. That predictability matters when you’re budgeting for life, vacations, kids, career changes, or just peace of mind.

2. Pursuing equity instead of paying a landlord

When you rent, that payment disappears every month. When you own, a portion of every mortgage payment can build equity—your ownership stake in the home. Over time, that equity can grow if your home appreciates in value. That’s how homeownership becomes a wealth-building tool.

3. Potential tax advantages

Depending on your situation, you may be able to deduct mortgage interest and property taxes. Always talk to a tax professional for specifics, but for many homeowners, there are real financial benefits beyond just appreciation.

4. The freedom factor

Paint the walls. Change the floors. Upgrade the kitchen. Hang that gallery wall. When you own your home, you don’t need permission to make it yours. And that feeling? It’s hard to put a price on.

The mortgage process (without the mystery)

When you work with our affiliated lender, HomeAmerican Mortgage Corporation (HMC; see licensing info), their goal is to make this process simple, predictable, and stress-free. You don’t need to memorize every mortgage term. You need to understand the flow.

Here’s what it really looks like:

Step 1: Pre-qualification

This is the conversation that sets everything up. They review:

- Credit report

- Income

- Assets

- Your comfort zone

Notice that last one. The question isn’t: “What’s the max you qualify for?” It’s: “What payment feels right for your life?” When you walk away from pre-qualification, you should feel clarity, not confusion.

Step 2: The loan application

Once you’re under contract on a home, you’ll complete a secure digital mortgage application. You’ll provide things like:

- W-2s

- Pay stubs

- Bank statements

- ID

It sounds like a lot, but most buyers are surprised at how smooth this stage is when they’re organized. HMC even has a way to securely link your payroll provider and asset accounts to an application portal. If you decide to opt in, it can really cut down on document gathering and speed up your approval process.

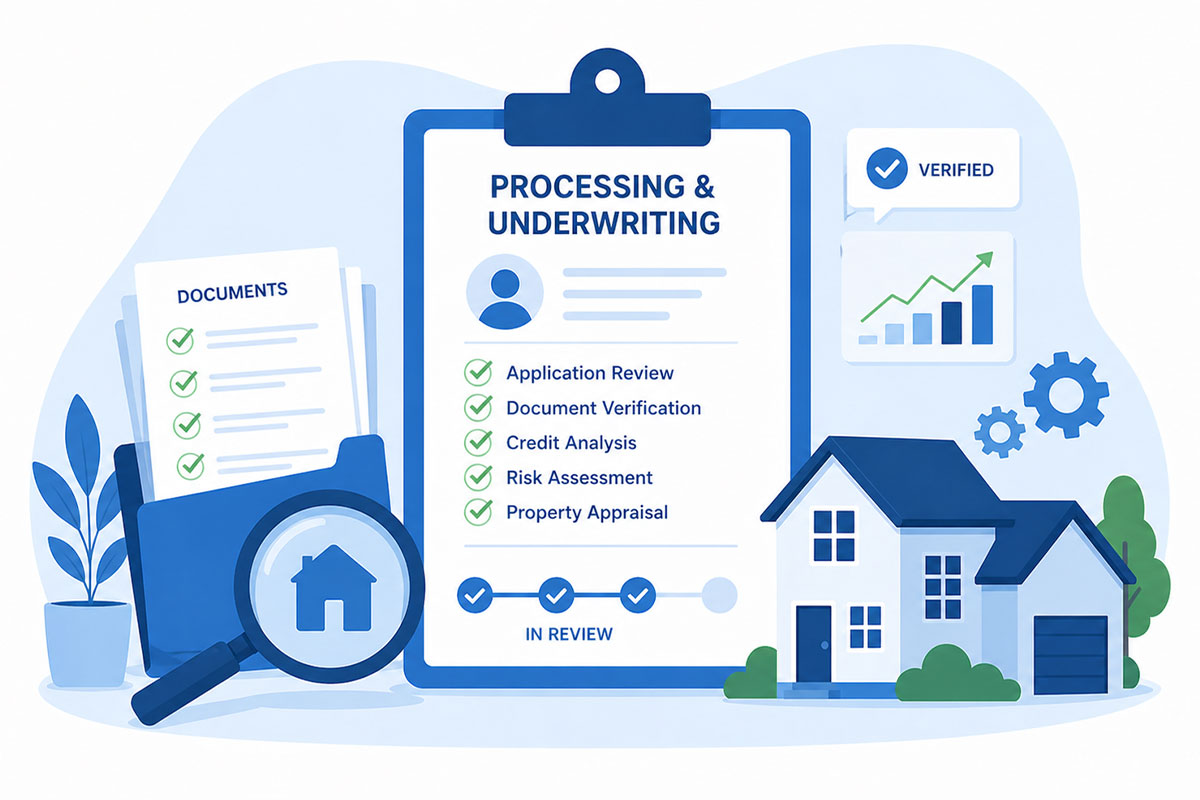

Step 3: Processing & underwriting

This is the behind-the-scenes review. Your employment is verified. Your income is calculated. Your credit and assets are confirmed.

Think of underwriting as the final double-check to ensure everything lines up properly. Most of this happens without your input, unless we need a document or clarification.

Step 4: Final approval

For new construction homes, final approval typically happens when the home is around 45–60 days from completion. At that point, your lender will refresh:

- Credit reports

- Bank statements

- Employment status

This is why we always say, avoid new debt before closing. No new cars. No financing furniture. No “we’ll just open one more credit card.” Stability is your best friend during this stage.

We know, this can be tough (especially if you’re closing around the holidays), but it will all be worth it when you’re celebrating in your brand-new home.

Step 5: Closing Day

You review your final numbers. You sign your documents. You get the keys. It’s the day everything shifts from “almost” to “officially yours.”

What lenders actually look at (It’s not as scary as you think!)

When applying for a home loan, lenders review three major categories: Credit. Income. Assets.

That’s it. Let’s break it down in real life terms.

1. Credit

Different loan programs have different minimum credit score requirements, but here’s what matters most:

- Paying bills on time

- Keeping credit card balances reasonable

- Avoiding new debt before closing

Credit utilization, how much of your available credit you’re using, plays a big role in your score. Keeping balances under 30% of your limit is generally a smart strategy.

2. Income

If you’re a W-2 employee, they look at your consistency. If you’re self-employed, they review tax returns. If you earn overtime or bonuses, they usually need a two-year history to count it. The key is stability. Lenders aren’t expecting perfection, they’re looking for responsible patterns.

3. Assets

Your assets show you have funds available for:

- Down payment

- Closing costs

- Required reserves (if applicable)

Acceptable sources often include:

- Checking or savings accounts

- Retirement accounts

- Gift funds (with documentation)

Lenders typically review the most recent 60 days of bank statements, and large deposits need to be sourced. That’s normal, not a red flag.

Why buying new construction can be a smart move

Buying new construction isn’t just a chance to get brand-new everything (though that’s a nice perk). It’s an opportunity to enjoy more personalization, efficiency, and sometimes financial advantages. Depending on the builder and timing, there can be:

- Closing cost assistance

- Interest rate buydown options

- Design center allowances

These offers can lower upfront expenses or improve long-term affordability. And when you use an afiliated lender, communication between the builder and lender is often streamlined. Everyone is aligned on product details, timelines, and milestones.

The goal is transparency, not pressure. It’s understanding what’s available and choosing what works best for you.

The buying timeline (from contract to keys)

Here’s what new construction buyers can typically expect:

Contract signing

You secure your home and submit your deposit.

Design Center appointment

You personalize finishes, colors, and upgrades.

Construction milestones

Foundation, framing, drywall, finishes—your home takes shape.

Loan approval status check

As completion approaches, documents are updated and approval is finalized.

Final walkthrough

You tour your finished home and ensure everything meets expectations.

Closing Day

You sign. You celebrate. You move in.

Most buyers say the process feels long at first, and then suddenly it’s move-in day!

So… What should you do first?

If you’re even thinking about buying, start here:

- Schedule a free pre-qualification

- Get a idea of what you’re comfortable financing

- Tour available communities

- Explore design options

- Ask questions, lots of them!

The goal is to set you up with a plan, not to pressure you. Whether you buy in 30 days or 12 months, preparation builds confidence. When you understand the homebuying process, mortgage approval, and financing options available to first-time buyers, everything becomes less intimidating.

This is about more than getting approved. It’s about stepping into a new chapter with clarity and excitement.

And when you’re ready, HMC will walk you through it, one simple step at a time.

8 Credit Score Management Tips

Applying for a mortgage soon? Our 8 Credit Score Management Tips could help put you on the path to better rates!